UNDERSTAND WHERE YOUR FEDERAL TAX DOLLARS GO

Let's explore where your tax dollars go, some of the ways tax filing may look different in 2022, and what you can do to prepare. Keep in mind, this guide is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and accounting professionals before modifying your strategy.

Before we dive into the upcoming tax brackets and what you can do to prepare for 2022, it can be helpful to understand precisely where the government allocates your federal tax dollars.

In 2021, the federal government spent $6.82 trillion, which equals 30% of the nation’s gross domestic product (GDP.) Further examination reveals that three significant areas of spending make up the majority of the budget.1

Medicare

Medicare accounted for $696.5 billion, or 10% of the budget, in 2021.1

Defense Spending

Another $754.8 billion, or 11% of the budget, was paid for defense and security-related international activities. The bulk of the spending in this category reflects the underlying costs of the Defense Department. This includes the cost of multiple defense initiatives and related activities, described as Overseas Contingency Operations in the budget.1

Social Security

Seventeen percent of the budget, or $1.1 trillion, was paid for Social Security, which provided monthly retirement benefits averaging $1,497 to 46 million retired workers. Social Security also provided benefits to 3 million spouses and children of retired workers, 6 million surviving children and spouses of deceased workers, and 10 million disabled workers and their eligible dependents.1,2

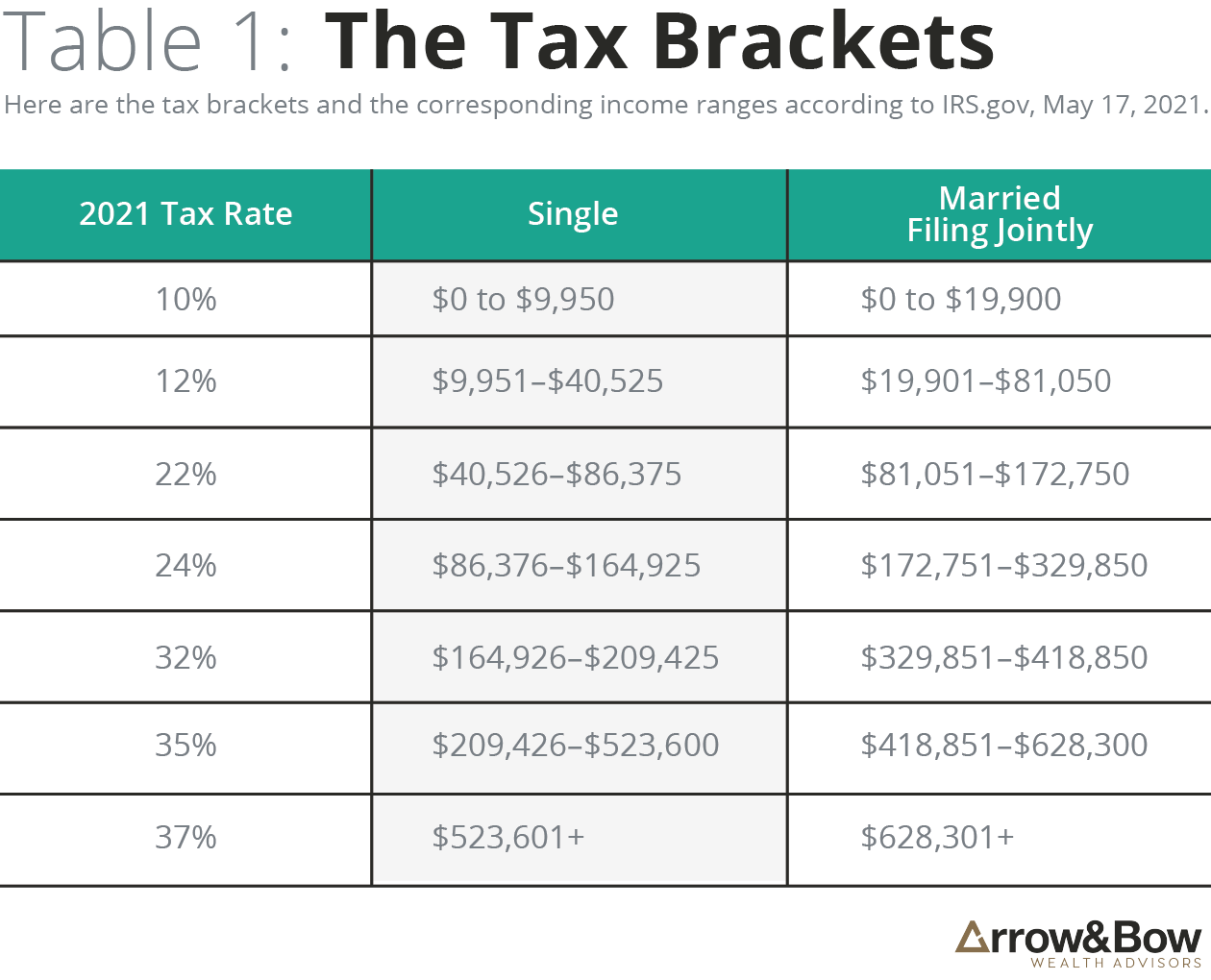

These modest changes to the tax brackets also mean that wage earners may fall into lower brackets. Here is one example. A single filer at $86,000 in taxable income would fall into the 24% bracket for tax year 2020. The filer would be in the 22% tax bracket in 2021.

These new rates are scheduled to expire in 2025 unless Congress acts to make them permanent. Exemptions also changed under the new tax code.

HOW TO PREPARE

Get a checkup: As a starter, the IRS urges taxpayers to conduct paycheck checkups.

The agency provides tools and resources to help you calculate the correct amount to have withdrawn from your paycheck.

The calculator may help you determine if your employer is withholding adequate amounts from your paycheck.

The calculator asks for your projected gross income, your current withholding number, the current amount of federal taxes withheld, and other paycheck-related questions.

The calculator leads you through various screens that require you to enter the requested numbers into boxes. The calculator looks similar to a tax-filing form.

The final figure: Once the calculator generates the estimated taxes you can expect to owe or be refunded, it offers suggestions on how to change your withholding amount or request that additional money be withheld from your check.

If the calculator shows you are projected to owe taxes at the end of the year, you may file a new Form W-4, Employee’s Withholding Allowance Certificate, following the guidance provided by the calculator. The IRS-provided calculator is designed to provide feedback based on certain assumptions. It is not intended to provide specific tax, legal, or accounting advice. The calculator is not a replacement for real-life advice, so please make sure to consult a professional before modifying your tax strategy.5

Suggestions may include changing the number of allowances you are claiming or requesting that your employer withhold additional money.

Taxpayers who receive pension income may use Form W-4P. Once completed, send the form to your payer if you are adjusting or making changes.6

WHAT DO YOU NEED TO HAVE TO USE THE CALCULATOR?

To generate a calculation, you will need to have these documents:

- A recent pay stub

- A copy of a completed Form 1040, which will helpyou estimate your income

The calculator will not ask you to provide personal or private information. It will, however, ask you the number of children you expect to claim for the Child Tax Credit and the Earned Income Tax Credit.

Taxpayers with more complex tax issues may follow the instructions in Publication 505, Tax Withholding and Estimated Tax.7

WHO SHOULD USE THE CALCULATOR?

The IRS urges taxpayers who have questions or concerns about changes in the tax code to use the calculator. Specifically, you may want to check your withholding if you meet the following criteria:

- Have a two-income household

- Have two or more jobs

- Work only part of the year

- Can claim child tax and other credits

- Have dependents who are 17 and older

- Itemized your deductions last year

- Are a high earner or have a complex tax return

- Received a large tax refund or paid a largetax bill for 2020

THE CHILD TAX CREDIT

In 2021, the Child Tax Credit was increased from $2,000 per qualifying child to $3,600 for children age five and under and $3,000 for children ages six through seventeen.8

There are two phase-out limits for the Child Tax Credit. The first phase-out limit can reduce the credit to $2,000 per child, which amounts to a potential $1,600 reduction for children five and under and a potential $1,000 reduction for children ages six through seventeen. This first phaseout reduces the Child Tax Credit by $50 for each $1,000 by which your modified adjusted gross income (AGI) exceeds the income threshold.

The second phase-out limit will further reduce the credit by an additional $50 for each $1,000 by which your modified AGI exceeds the income threshold. The thresholds for each phaseout limit are shown below.

There still remains a tax credit of up to $500 for other dependents who may not qualify for the Child Tax Credit. Children you plan to claim as dependents must have Social Security numbers prior to the due date of your tax return. Children who do not have Social Security numbers but have individual taxpayer identification numbers may be claimed under the new credit for other dependents.

PREPARING FOR THE TAX SEASON

Planning well in advance of the tax season may help better prepare you for the unexpected. Here are several reasons to begin planning early:

- Your home, job, or relationships changed in 2021

- You need to start saving money if you may owetaxes.

- You want to ensure you qualify for tax deductions

You can make changes throughout the year to ensure that your tax preparations go smoothly.

In particular, you can make periodic assessments of your paycheck withholdings so that you will get a refund or can reduce or eliminate your tax burden.

You should keep track of and store your tax and other financial records to avoid delays or frantic preparations as the filing deadline approaches. Records may include W-2 forms, canceled checks, certain receipts, and previous-year returns.

Here is a list of other items to start gathering:

- Pay stubs

- Mortgage payment records

- Closing paperwork on home purchases

- Receipts for items or services you may want toclaim as itemized deductions

- Records on charity giving and donations

- Mileage logs on cars used for business

- Business travel receipts

- Credit card and bank statements to verify deductions

- Medical bills

- 1099-G forms for state and local taxes

- 1099 forms for dividend or other income

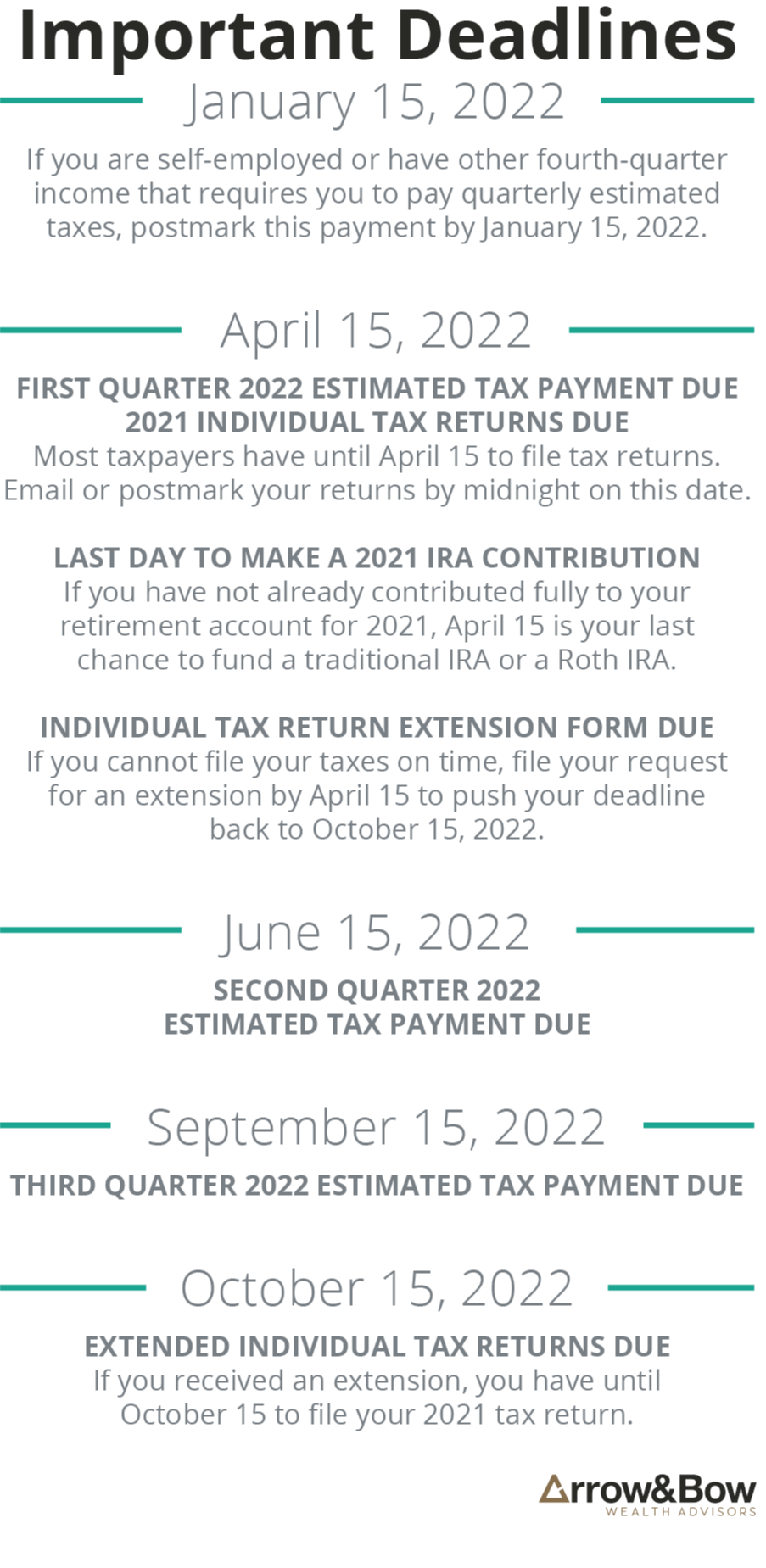

During the first few months of 2022, make sure you receive your W-2 and 1099 forms as well as other tax documents. Leave adequate time to collect documents and prepare to file your taxes prior to the April 15, 2022 deadline.

TIGHTENING THE NUTS AND BOLTS

Although the 2020 tax season is more than six months behind us, the final months of 2021 provide taxpayers with some unique opportunities to avoid unpleasant surprises and scrambling as the finish line draws near.

Here are some ways to prepare this year for next year’s tax season:

Look at last year: Take one more look at last year’s return. In the months ahead, you may still have the opportunity to contribute more to your retirement plan, which may lower your taxable income.

Donate to charity: How about “bunching” your charitable donations?

Bunching provides you with the ability to optimize your deduction allowances by making two or more years’ worth of charity donations in one year.

Let us say you are married, you plan to itemize your deductions, and you plan to make $15,000 in annual donations. By donating $30,000 in one year andskipping the next, you may be able to qualify for ahigher deduction.9

Review capital losses: If you are investing in the financial markets, you may want to consider deducting capital losses; you have the opportunity to claim deductions if you experienced losses.

You can claim losses only if they exceed capital gains. You are allowed to claim the difference of up to $3,000 per year if you are married filing jointly or $1,500 if you are filing separate returns. Net losses that exceed $3,000 can be carried over into future years.10

Deductions for capital losses can only be applied to investment property sales but not to the sale of investment property that was held for personal use.

Get organized: Find a place to store your tax documents until it is time to prepare to file. A good record-keeping system may alleviate concerns later as the deadline gets closer.

If you have your documents or prior-year returns stored on your computer, make sure you back them up on a thumb drive or other device or system in case your computer is hacked or stolen.

Consider other taxes: Keep an eye on local and state government requirements that may affect your specific tax situation.

HOW LONG?

The IRS provides recommended timelines for retaining financial documents:11

- You should keep your tax records for three years if #4 and #5 below do not apply to you.

- You should keep records for three years from the original filing date of your return or two years from the date you paid your taxes. Select whichever is the later date. This is if you claimed a credit or refund after you filed your return.

- You should keep your records for seven years if you claimed a loss from worthless securities or a bad debt deduction.

- You should keep your records for six years if you failed to report income that you should have, and the income was more than 25% of the gross income listed on your return.

- Keep records indefinitely if you do not file a return.

- You should keep employment tax records for at least four years after the due date on the taxes or after you paid the taxes. Select whichever is later.

I hope you found this to be educational and informative. You may incorporate the principles and tips in this report into your tax preparation strategy. Planning well in advance may enable you to take advantage of the opportunities and benefits available under the new tax code. Discussing your unique situation with both a financial professional and a tax professional may help you make the best choices as tax season approaches. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult with legal or tax professionals with expertise in this area for specific information regarding your situation. If you or anyone close to you would like to discuss how to manage your financial situation, please give our office a call to schedule a consultation.

FOOTNOTES, DISCLOSURES, AND SOURCES

Securities and Advisory services offered through LPL Financial. A registered investment advisor. Member FINRA & SIPC. The LPL Financial representative associated with this website may discuss and/or transact securities business only with residents of the following states: AL, AR, CA, CT, DC, FL, GA, IL, KY, LA, MD, MN, NC, NY, OH, PA, SC, TX, VA, WY

These are the views of FMG Suite, LLC, and not necessarily those of the named representative, broker/dealer or investment advisor, and should not be construed as investment advice. Neither the named representative nor the named broker/dealer or investment advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial professional for further information.

1. USASpending.gov, 2021

2. SSA.gov, 2021

3. IRS.gov, May 17, 2021

4. ConsumerismCommentary.com, April 5, 2021

5. IRS.gov, September 29, 2021

6. IRS.gov, June 10, 2021

7. IRS.gov, April 13, 2021

8. IRS.gov, September 23, 2021

9. IRS.gov, August 18, 2021

10. IRS.gov, March 12, 2021

11. IRS.gov, August 5, 2021